The new tax reform came into force on 1 January 2024. One of the changes in the tax reform is the transfer tax known as (ITP) lowers the general rate of 10% at 9%.

What is the transfer tax?

Known as ITP, this is a tax that has to be paid by the buyer to the Treasury when second-hand real estate transactions are carried out.

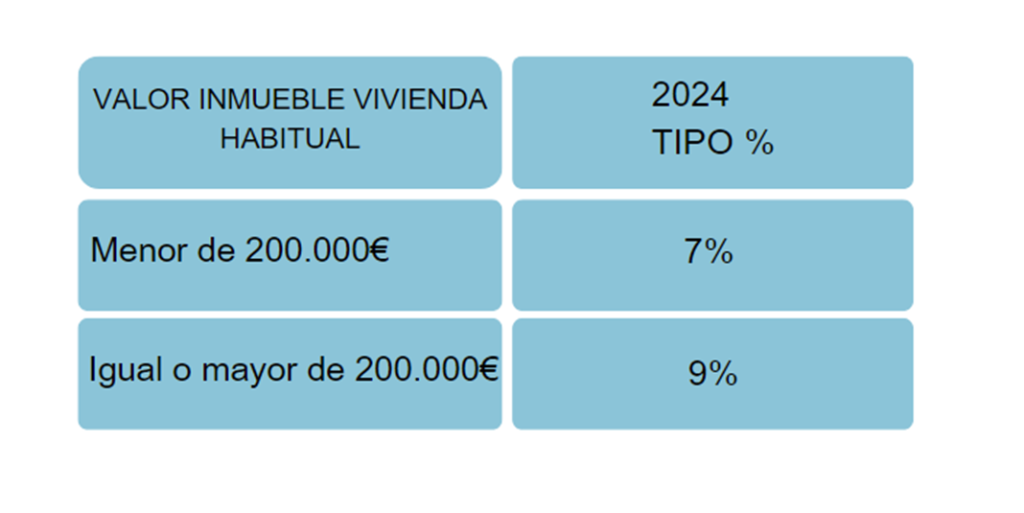

If the dwelling is to be used as a principal residence and the value of the property is less than €200,000 the percentage is 7% and if the value is equal to or greater than 200.000€ the percentage is 9%:

General type 9%:

In general, in the transfer of movable property, as well as in the creation and transfer of rights in rem relating thereto, except in the case of rights in rem as security, the rate applicable shall be the following rate from 9%

Reduced rates 4%:

If the value of the property does not exceed 300,000€ the reduced rate is the 4% if you meet the following requirements as long as the property is intended for your main residence:

- Have, at the date of acquisition of the property less than 36 years old compliments

- Person with physical, mental or sensory disability who is legally considered to be a person with a common disability with a degree of disability equal to or greater than 33 per cent and less than 65 per cent.

- To be considered as the holder of large family or spouse of the same or of single-parent family by virtue of Decree 26/2019 of 14 March.

- In transmissions of public housing which do not benefit from the exemption provided for in Article 45 of Royal Legislative Decree 1/1993

- When the dwelling is located in Municipalities at risk of depopulation

Reduced rates 5%:

For home purchases not exceeding €300,000 that are to be subject to immediate refurbishment, and must meet the following requirements:

- In the public deed The sale and purchase agreement shall be concluded by go on record that the dwelling is to be the subject of immediate rehabilitation

- The total cost of the rehabilitation work shall be at least 25% of the purchase price of the dwelling recorded in the deed or in the corresponding administrative or judicial document. The amount paid in the invoices for VAT tax will not be taken into account for the computation of the total cost of the refurbishment work when the purchaser is a VAT taxable person and can deduct it.

- Living in the dwelling for three years after completion of the work

- The estimated timeframe for the duration of the works cannot be longer than 18 months from the date on which the tax becomes chargeable

It excludes of the concept of home renovation works carried out by the homeowner himself without the participation of professional builders.

Within a maximum period of one month after 18 months from the accrual date, the taxpayer must submit the following documentation to the competent tax office or settlement office of the Mortgage District:

- Invoices rehabilitation-related

- Municipal building permit of rehabilitation of the dwelling stating the amount thereof